SMEconomics Overview

- Australia’s economy looks like it will recover the loss of income and employment from the pandemic over the first half 2021. Our success in fighting the virus has combined with new innovative economic policies to facilitate a strong rebound in activity.

- Growth will be harder to come by in 2021 although the foundations of a sustained expansion of economic activity are being laid. Strong demand for residential housing will translate into new building activity. Business confidence and investment intentions are on the rise.

- The end of JobKeeper, the normalisation of Jobseeker and the end of the loan deferrals program will be a drag on the economy as winter approaches. It looks like the economy has enough momentum to absorb the disruption to employment and spending.

- Another headwind will be low population growth in 2021. International border closures have put a halt to the normal flow of migrants to Australia. The effect will be exacerbated in the major cities where a larger number of people than usual are leaving for regional areas.

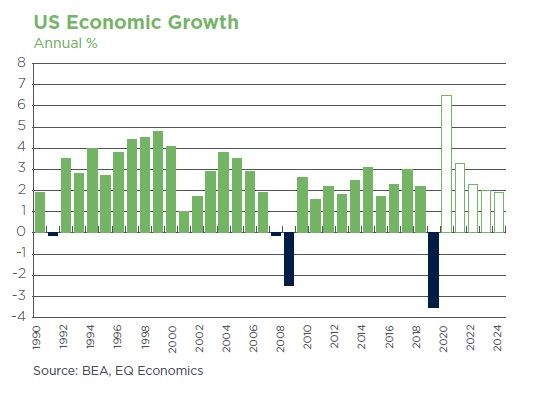

- The world’s two biggest economies are set to grow at very high rates in 2021. Economic growth in the United States could exceed 6% while the Chinese economy could expand by up to 10% after a soft patch in 2020. Both governments have enacted large stimulus programs which will boost spending in their economies this year. This will generate trillions of dollars in new economic activity around the world helping to drag other economies onto a higher growth trajectory.

- The global rollout of vaccination programs is picking up pace as 2021 progress. The US and the UK are well advanced as of March, but many countries are lagging. Australia is in an enviable position with virtually no community transmissions, time is on our side. The government expects most people to have had the jab by October. Internal border and other domestic restrictions are being eased.

- The housing market is being buoyed by low interest rates, rising employment and a shift in preferences towards detached housing in the suburbs and regional Australia. House price growth has been phenomenal in the first few months of 2021 with the period between Australia Day and Easter potentially one of the most rapid on record.

- The stronger than expected rebound in economic activity has financial markets worried about a resurgence of inflation. Central banks around the world, including the RBA, are signalling near zero cash rates for 3 years. Bond markets are not so sure with long-term interest rates rising in recent months.

- The outlook for inflation is highly uncertain with both inflationary and deflationary forces buffeting the global economy. Central banks will allow inflation to run higher from current low levels. Even if we see higher inflation it is unlikely to motivate central banks to hike rates anytime soon.

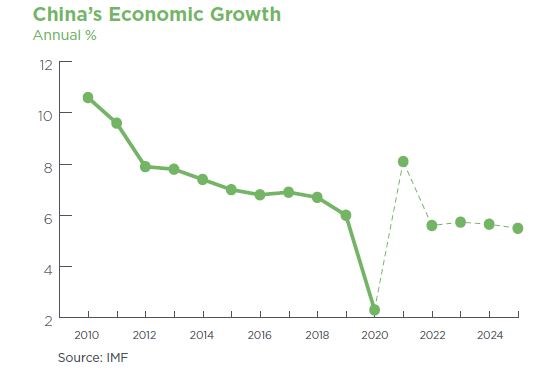

- China has navigated the pandemic incredibly well from both a health and economic perspective. Despite an expectation of very strong growth this year, the Chinese Government remains focused on the long game. It is the quality of growth that concerns Chinese officials with the quantity less important than it was in the past.

- Economic success has opened the door for the Australian Government to repair its budget position much more quickly than originally thought. There is much more work to be done to get Australia’s government finances back on a sustainable footing. The trick is calibrating the withdrawal of government spending with the recovery of private sector activity, not an easy task. The next phase of fiscal consolidation will have to wait until the economic upturn is firmly established, which is probably another year away.

The global economic recovery will be powered by the world’s two biggest economies as government stimulus drives strong growth in the US and China in 2021.

The global economy is set to experience one of its best years of economic growth in decades driven by big improvements in the performance of the world’s two biggest economies, the United States and China. The US was once described as the engine of the world economy. We now have two engines of global economic growth and they both look set to generate a considerable amount of new business for the world economy over the next two years.

China is expected to register growth of 8% in 2021 (see China Focus on page 7), up from 2.3% in 2020. This will be the strongest growth in a decade. The US is not far behind with forecasts for GDP growth in 2021 now at 6.5%, an extraordinary outcome for an economy that has averaged less than 2% growth since 2000. Both economies are benefiting from big government stimulus programs with President Biden’s US$1.9trn package passing into law in March.

Europe has continued to struggle with the coronavirus in the first quarter of 2021 despite vaccination rollouts and heavy restrictions being imposed in many countries. Europe is suffering from the spread of new strains of COVID-19 which vaccination programs have not been quick enough to suppress. The European recovery has been delayed and is likely to be later and less vigorous than what we will see in many other advanced economies.

A resurgent US to lead the global recovery in 2021 and 2022

US President Biden’s stimulus package is one of the most significant pieces of legislation in the US in a generation. At US$1.9trn, the package is worth about 8.5% of GDP. It is only slightly smaller than the initial pandemic stimulus plan of US$2.2trn delivered by President Trump in March 2020.

To give some context, the package is the equivalent of A$2.5trn, that is, 130% of Australian GDP. In historical terms, the Congressional Research Service in the US estimates that World War Two cost the US government US$4.1trn in 2020 dollars. The cost of fighting the COVID-19 pandemic will be at least US$5.5trn.

Many of the key programs are targeted at low and middle income earners through direct cash payments, income tax credits for families, health care support and paid leave. The biggest impact will be on low income households which has the dual benefit of addressing chronic inequality issues as well as acting as a very effective short-term boost to economic activity. Low income support payments tend to be spent.

The US consumer markets are the largest in the world. Total US consumption was over US$14trn in 2020 with imports of consumer related goods and services topping US$1trn. The US imports consumer products from over 200 countries around the world.

When the US economy is growing vigorously, everyone benefits as rising demand triggers new investment in other countries, which in turn filters around the global economic system.

A feature of the global recovery from this pandemic will be the divergence of recovery rates. Many emerging economies and some countries in Europe will lag the US and China. But as the two engines of global growth fire up this year, they should drag the whole world along with them over the next couple of years.

A lift in investment across the economy will ensure a sustained economic expansion for Australia.

Investment is central to a prolonged expansion of economic activity. Investment in business equipment, housing and other construction is what generates an upswing in the economy, creates jobs, higher incomes and spills over into the broader services and manufacturing sectors.

Every economic cycle has its own characteristics reflecting social and economic changes within the community. This economic cycle is likely to be influenced by the changes to behaviour brought on by the coronavirus pandemic.

While many of the behavioural shifts we made to navigate the pandemic will prove temporary, there are also likely to be ways of doing things that have changed permanently. The pandemic pushed a higher share of the economy online, from retail trade to the acceleration in the trend to work from home.

Working from home has been thrust upon many industries, forcing both employer and employee to adapt to new work practices. Technology has been at the centre of this shift, enabling people to work remotely while collaborating and engaging with team members. There is now a much wider acceptance in both cultural and practical terms of remote working.

Various studies have attempted to estimate the new normal. Estimates for those in industries and jobs where remote working is practicable generally range from 2 to 3 days a week (at home). If this is right the implications for the upcoming economic cycle are important.

New investment will flow to boost the housing stock. Detached housing in the suburbs will benefit at the expense of inner-city apartments. Regional areas could experience a sustained inflow of new residents as people spend more time working from outside of the cities. This will raise income levels in regional centres and drive new business investment and hiring.

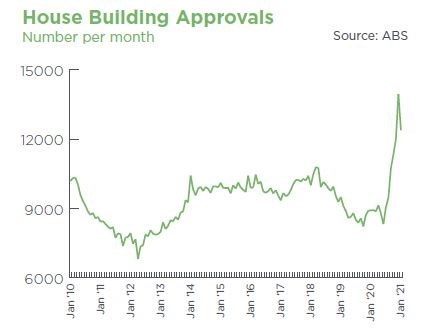

All the pieces are in place for a lift in housing construction (see Housing Update, page 5). Council approvals for the building of houses and renovations have increased strongly over the second half of 2020. Approvals for apartment construction remain weak early in 2021.

Commercial construction should continue to expand as a lift in infrastructure spending and a surge in demand for industrial property are driving activity in 2021. However, office and retail markets are not expected to perform as well due to the shift to the digital economy.

The pandemic will shape investment within the economy over the years ahead.

Outside of construction, business investment is going to have to lift if we are to entrench the recovery from COVID-19 into an on-going economic expansion. Recent data has been encouraging. Not only is business confidence at very high levels, non-mining business investment in plant and equipment jumped 8.4% in the December quarter of 2020, the highest quarterly rate of growth in a decade.

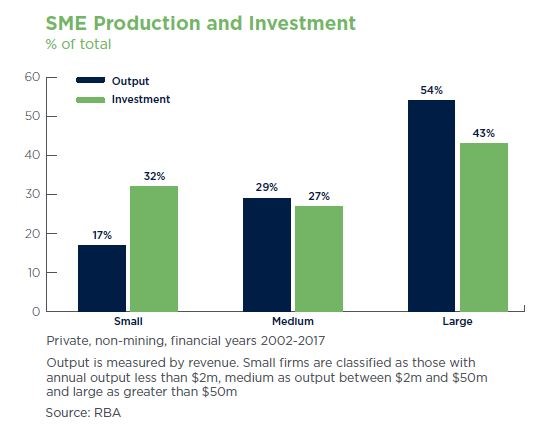

RBA analysis shows that small businesses are crucial to business investment in Australia. Small business accounts for 17% of output (production) across the economy yet they make up 32% of non-mining business investment. The RBA identified four characteristics of small business investment and why it is important to the economy: drives innovation, generates new ideas, stimulates competition, and supports employment.

The message: Get small business investing and you will get the economy moving!

The housing market upswing has a long way to run.

One of the most remarkable features of the economic recovery from COVID-19 has been the rapid rise in house prices across the country. The increase in demand for housing is mostly coming from owner occupiers. First home buyer and ‘upgrader’ numbers are rising, and they are taking on bigger mortgages to compete for a limited supply of stock on the market. The monthly value of new mortgages taken on by owner occupiers hit a record high level of more than $20bn early in 2021.

Investors are lagging the market upswing with a modest increase in activity from the depths of the pandemic induced downturn last year. Investor activity is still well below the high point seen in the housing boom of 2015 to 2017 largely the result of falling rents in many markets and the potential for deferred loans to drive a surge in foreclosures after the program ends in March.

The strong rise in house prices should translate into a lift in house building in 2021.

Why has the housing market recovered so strongly?

-

The economic recovery has been quicker and stronger than anyone expected. This has translated into rising employment and consumer confidence.

-

Mortgage interest rates have fallen to levels never seen before. Debt servicing is at the lowest level in decades and is allowing people to compete aggressively in the market.

-

There is a pent-up demand for housing that existed prior to the pandemic. Housing had experienced a slowdown from 2017 through to 2019 and was set to turn higher when the pandemic struck.

-

The pandemic has had a profound effect on how people think about housing. Lockdowns and restrictions combined with the need to work from home have transformed many people’s views on what they want from housing. Specifically, this has resulted in increased demand for detached housing and a shift towards the suburbs and regional areas.

The demand from owner occupiers should continue to grow as economic activity and employment recover further. Demand is outstripping supply, driving higher prices. High price growth should continue until there is a meaningful increase in supply. The construction of new houses should accelerate in 2021 and bring new supply to the market over the second half of the year.

The missing ingredient in the housing story is investors. Despite the negative impacts from the pandemic, low interest rates and expensive equity market valuations should eventually translate into more investor activity over the year ahead. The post COVID normal should see investors accept a lower rental yield given the new lower level of interest rates. Owner occupiers are clearly driving the first phase of recovery in housing markets, but it is likely to be investors that take the market to the next level sometime later this year or next.

The RBA has stated unequivocally that they will not be responding to rising house prices with higher interest rates. The message from the RBA could not be clearer; interest rates will remain at the current rock bottom levels for at least three years. This will be an on-going source of support for Australian housing markets.

Regulators will be watching lending standards, particularly for investors should they return to the market in a substantial way. Just like we saw in 2017, the Australian Prudential Regulatory Authority (APRA) will not hesitate to introduce restrictions on mortgage lenders should they see higher risk lending becoming widespread.

Is inflation making a comeback?

Most central banks hope to achieve an inflation rate of about 2%. It is a bit like Goldilocks: too much inflation is not a good thing but too little can get you into trouble as well. Inflation needs to be ‘just right’. In the US ‘just right’ is an inflation rate of about 2% while here in Australia the RBA and government have agreed that we should be trying to get inflation of somewhere between 2% and 3%.

For the last 10 years inflation in most countries has been below the rate that central banks are targeting. Low inflation or deflation (falling prices) can be a disaster for an economy with high debt levels, which is almost every country in 2021. If low inflation leads to falling wages and revenues, then the outstanding debt will become more of a burden because you must dedicate more of your income to pay it off.

Central banks in just about every advanced economy are attempting to generate higher inflation. They have taken short-term interest rates to zero and are using Quantitative Easing (QE) programs to buy bonds and push down long-term rates as well. In a nutshell central banks are printing more and more money but none of it seems to be working.

The reality is that extra money in the financial system is escaping into the economy via higher asset prices, that is, the value of assets like equities and property are rising sharply, not consumer prices, and not wages.

Inflation pressures are isolated and unlikely to emerge in a substantive way for a few years yet.

The pandemic has had a big impact on industry and supply chains, and is creating pockets of inflation pressures. With central banks upping their money creation some commentators are worried that we may be due for a burst of inflation.

There are many factors putting upward pressure on inflation right now. Commodity prices have been rising. Rising trade barriers are inflationary and supply chain disruptions are creating a shortage of certain products, which could see prices rise.

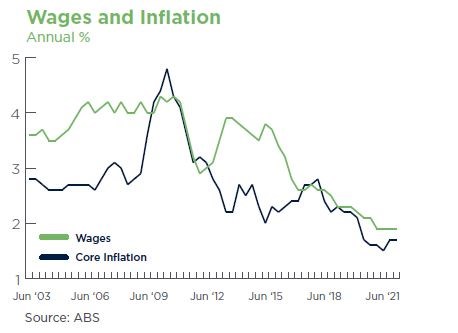

Offsetting this is the fact that the biggest input into production across the economy, wages, are not increasing all that much. This is why the RBA repeatedly talks about getting wage growth up in order to put upward pressure on inflation across the economy.

Wage growth in Australia is well below a level that will spur higher inflation. If inflation is to run at 2-3% consistently, then wages, as the largest cost component in the economy, must increase by at least 3% each year. At present, wage growth is 1.4% and does not look like rising to 3% for many years.

When I speak to SME’s the high cost of labour is an almost universal concern. It is a striking feature of the current Australian economic landscape how much of a problem high labour costs are for business yet how much of a concern that low wage growth is for monetary policy.

Central banks think that if they can drive the economy hard enough and get unemployment down to very low levels, eventually businesses will be forced to pay higher wages. The problem with this reasoning is that higher wages may not necessarily translate into higher inflation if businesses are unable to put their prices up.

One of the most important reasons that inflation has been low is that consumers are much more resistant to price increases than ever before. If we get higher wages yet business can’t pass it on to consumers then all we will get is weaker profitability and less business investment.

Until consumer resistance to price increases fades, we are unlikely to get permanently higher inflation. But that is not necessarily a bad thing. A surge of inflation that leads to higher interest rates will be as damaging, if not more so, than the experience we have had of prolonged low inflation.

China Focus: Beijing remains focused on the long game.

Prior to the COVID-19 pandemic the Chinese authorities were squarely focused on the final stages of transforming the economy into a modern, services-based economy. This involved less reliance on manufacturing and heavy industry and more activity coming from domestic consumption and the services sector.

The Chinese policy response to the pandemic was out of a long established play book. Government led infrastructure spending driving domestic manufacturing and construction. This traditional government stimulus approach worked well to arrest the downturn in economic activity early last year, but paused the long-term transition of the economy towards services.

The pandemic has hurt Chinese consumer spending, and the service industry in particular, as it has done all around the world. While the government must entrench the economic recovery from COVID-19, which may mean continued support for traditional stimulus programs, it is also trying to promote consumer spending and the growth of the service industries.

The reality is that China has navigated the pandemic extremely well and is set to grow the economy at an incredible 8% rate this year, higher than the recently announced growth target for 2021 of ‘above 6%’.

The recently released 14th Five Year Plan maps out the government’s economic and social priorities. It is quite clear that China’s economic strategy is shifting away from the quantity of growth to the quality of growth.

The message from the new 5 year plan is that technology, environmental responsibility and higher value industries are the priority. The government is also keen to moderate fiscal deficits and government debt, which have surged through the pandemic.

China has navigated the pandemic well, but economic challenges remain, not least, the need to get more of its economic activity from consumer spending and the service sector.

The implication is that the real growth opportunity over the next decade is likely to come from markets linked to the rapidly emerging middle class and the provision of domestic services. The Chinese are technology hungry and will welcome industry that bring new ideas from banking and finance to health and aged care. Australia has benefited greatly from the Chinese government response to COVID-19. Despite numerous trade sanctions on Australian products, our exports to China have hit a record high in 2020. That is largely the result of higher volumes and prices for our iron ore. Many of our exports to China have slumped due to trade restrictions, while others that are deemed important to China continue to grow.

The future of Australia’s trade with China is not at all clear. The opportunities that a rapidly growing middle class offers are vast although recent events put a cloud over market access. These trade restrictions have done considerable damage to the attitude of many Australia businesses to the Chinese market.

Many exporters are looking to other high potential markets in Asia such as India, Vietnam and Indonesia which, although lagging China’s spectacular development of the past 20 years, are still on a high growth trajectory.

Government Budget focus shifts to fiscal consolidation as the economy improves.

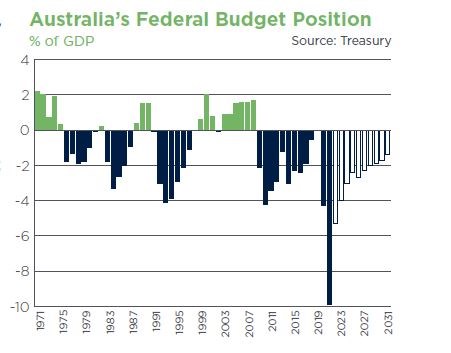

Australian governments have spent over $300bn fighting the COVID-19 pandemic. Economic stimulus and support programs have worked, playing a major role in establishing a fast V-shaped recovery from the pandemic.

For the Federal government, the focus must shift to fiscal consolidation to ensure that the burden we place on future generations, through the build up of debt, is minimised. It is simply unfair on future taxpayers to keep piling up debt now that the economic crisis has passed.

The Federal government will bring down the 2021/22 Budget in early May. Since the last (delayed) Budget was released in October the federal government has been squarely focused on the first phase of fiscal repair, that is, the unwinding of emergency policy measures such as JobKeeper.

The government’s strategy to recover from the economic impact of COVID-19 has always been about supporting a business led recovery.

Thankfully, all has gone pretty well from an economic and health perspective. The winding up of JobKeeper will result in one of the biggest contractions in government spending in history. The deficit is expected to be $198bn in the current financial year, largely due to the $90bn cost of the JobKeeper program. As emergency economic support programs are wound down, the Federal government is expecting the deficit to shrink to $109bn in 2021/22.

A deficit of $109bn is still very large by historical standards. At 5.3% of GDP, it is roughly the size of the deficits Australia ran through the worst of the Global Financial Crisis in 2008/09. Even though we have a recovery underway we still have a very large deficit.

There is much more work to be done to get Australia’s government finances back on a sustainable footing. The trick is calibrating the withdrawal of government spending with the recovery of private sector activity, not an easy task but one that they have done well thus far.

The Federal government will be confident that the economy is on the right path as it prepares for the May Budget. And the budget is likely to be in better shape than previously expected largely because the strong economic recovery will have generated higher tax revenues than forecast.

That is good news because it is too early to undertake a further fiscal consolidation in Australia. The recovery might be well underway but the full implications of the end of JobKeeper are still largely unknown and will not be known as the Federal government’s Budget is put together in April. We will have to wait until late May, if not June, to be confident about the post JobKeeper economy.

If the economic recovery quickly turns to economic boom, a good problem to have, the government can implement a quicker fiscal consolidation at the Mid-Year Economic and Financial Update (MYEFO) later this year. If they tighten up too quickly and the economy is impacted, it will be very hard to re-establish the strong economic momentum we now have.

With the economy on track, the government will rightfully be careful not to splurge on too many new measures at the upcoming Budget, and the PM has signalled as much. That said, they should be careful in pulling back too much. The second phase fiscal consolidation can wait until next year when the medium-term economic outlook becomes clearer.

Disclaimer

This document has been prepared by Judo Bank Pty Ltd ABN 11 615 995 581 AFSL 501091 (“Judo Bank”). Any advice contained in this document has been prepared without taking into account your objectives, financial situation or needs. Before acting on any advice in this document, Judo Bank recommends that you consider whether the advice is appropriate for your circumstances.

So far as laws and regulatory requirements permit, Judo Bank, its related companies, associated entities and any officer, employee, agent, adviser or contractor thereof (the “Judo Bank Group”) does not warrant or represent that the information, recommendations, opinions or conclusions contained in this document (“Information”) is accurate, reliable, complete or current. The Information is indicative and prepared for information purposes only and does not purport to contain all matters relevant to any particular investment or financial instrument. The Information is not intended to be relied upon and in all cases anyone proposing to use the Information should independently verify and check its accuracy, completeness, reliability and suitability and obtain appropriate professional advice. The Information is not intended to create any legal or fiduciary relationship and nothing contained in this document will be considered an invitation to engage in business, a recommendation, guidance, invitation, inducement, proposal, advice or solicitation to provide investment, financial or banking services or an invitation to engage in business or invest, buy, sell or deal in any securities or other financial instruments.

The Information is subject to change without notice, but the Judo Bank Group shall not be under any duty to update or correct it. All statements as to future matters are not guaranteed to be accurate and any statements as to past performance do not represent future performance.

Subject to any terms implied by law and which cannot be excluded, the Judo Bank Group shall not be liable for any errors, omissions, defects or misrepresentations in the Information (including by reasons of negligence, negligent misstatement or otherwise) or for any loss or damage (whether direct or indirect) suffered by persons who use or rely on the Information. If any law prohibits the exclusion of such liability, the Judo Bank Group limits its liability to the re-supply of the Information, provided that such limitation is permitted by law and is fair and reasonable.

This document is intended only for clients of the Judo Bank Group, and brokers who refer customers to the Judo Bank Group, and may not be reproduced or distributed without the consent of Judo Bank.

The Information is governed by, and is to be construed in accordance with, the laws in force in the State of Victoria, Australia.